KLAS Contact

Contact KLAS

Contact KLAS

2024 BEST IN KLAS

2024 BEST IN KLAS

Preferences

Related Series

2021

2014

2013

2013

2012

2011

ACO Payers 2014

Le Tour de Risk

Author

Mark Allphin

Providers are moving steadily down the path of value-based care, but they vary in their readiness to take on more risk. Fortunately, commercial payers offer a range of “rides” that fit providers’ different needs, from comfortable transitions to trail-breaking endeavors. Based on conversations with 23 providers about 43 risk sharing agreements, this study examines the roles that five top national payers are playing in helping providers progress in the new world of accountability.

WORTH KNOWING:

SLOW EVOLUTION TOWARD DEEPER RELATIONSHIPS

As providers and payers reinvent their relationships, a legacy of distrust means slow progress. When providers rated their payers in five areas on a scale of 1.0 to 9.0, no one area received an average score above 6.6—the equivalent of a C- grade.

COMFORTABLE TRANSITIONS

Providers new to accountable care gave Cigna and WellPoint the highest rating for collaboration, a reflection of the payers’ low-risk, low-cost programs that guide providers step by step without requiring large technology investments or major organizational changes.

TRAIL-BREAKING ENDEAVORS

Providers described Aetna as an innovative partner. Many of these providers already have population health experience and tool sets and are in a process of reinvention, often creating their own co-branded products for local employers. They rated their Aetna relationships highest for flexibility and profitability.

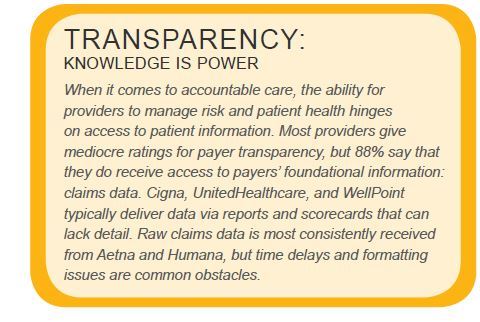

TECHNOLOGY TAKES A BACKSEAT

While payers like Aetna, Humana, and UnitedHealthcare have made large investments in technology firms, only a handful of providers have adopted their tools. Providers most value payer services. Cigna,UnitedHealthcare, and WellPoint providers rely heavily on risk stratification and care-gap reporting. Aetna and Humana customers prefer access to raw claims data so they can use their own tools.

AFFORDABILITY CONCERNS PROVIDERS

Most providers receive per-member per-month assistance to hire care-coordination staff, but those funds are generally insufficient. Considering their out-of-pocket costs, providers rated the affordability of their relationships between 5.2 and 6.3 out of 9.0. Humana rated lowest, as some of their providers use Humana as a hired plan administrator rather than a partner.

PROFITABILITY IS A MIXED BAG

Many providers declined to rate the financial returns of their at-risk contract, saying it is too early to tell. Aetna, Cigna, and UnitedHealthcare providers had enough experience to give an early rating, but they see profitability very differently. Aetna providers, who had the most at risk, rated profitability highest, at a 6.8. Cigna and UnitedHealthcare providers, with more restrictive and prescriptive programs, gave ratings of 5.4 and 4.9, respectively.

Payer Profiles Card

| PAYER | AVG.# PATIENTS | RISK ARRANGEMENTS | PROFILE |

|---|---|---|---|

| CIGNA | 9K | Mainly upside shared savings | Largest national program. Prescriptive relationship includes welcome guidance and hand-holding, but minimal financial reward for succesful providers. |

| WELLPOINT | 10K | Upside shared savings & performance payments | Relative newcomer to accountable care. Most collaborative payer for hand-holding. 100% of providers received PMPM fnancial assistance. Greatest transparency via care-management and performance reports. |

| HUMANA | 13K | Upside shared savings & captation | Providers more likely to take on majority of fnancial risk within bounds of Medicare Advantage programs. Humana often seen as a contracted administrator. No mention of Humana’s investments in HIE and care-management software. |

| UNITEDHEALTHCARE | 44K | Upside shared savings & performance payments | Largest patient populations as UnitedHealthcare expands existing, traditional relationships to include some risk. Low fexibility, risk, financial reward. UnitedHealthcare Group's subsidiary Optum plays only minor role. |

| AETNA | 27K | Upside & downside shared savings | Most cited as “partnership.” Often customized, cobranded health plans. Healthagen subsidiary sells tools and services, but typically not included as part of payment contract. Highest provider proftability so far. |

This material is copyrighted. Any organization gaining unauthorized access to this report will be liable to compensate KLAS for the full retail price. Please see the KLAS DATA USE POLICY for information regarding use of this report. © 2024 KLAS Research, LLC. All Rights Reserved. NOTE: Performance scores may change significantly when including newly interviewed provider organizations, especially when added to a smaller sample size like in emerging markets with a small number of live clients. The findings presented are not meant to be conclusive data for an entire client base.